熱門資訊> 正文

Weekly Review: Municipal Bond CEFs - The Uncertain Market Environment Gave A Positive Impulse To The Sector

2019-05-23 05:35

- Neuberger Berman New York Intermediate Municipal Fund, Inc.(NBO) 0

- Invesco Advantage Municipal Income Trust II(VKI) 0

- Neuberger Municipal Fund Inc.(NBH) 0

The investors changed their focus to safer assets due to the uncertainty around the trade deal and the volatility on the stock market.

We continue to follow the most important yields and municipal/Treasury spread ratio.

Most of the funds from the sector are traded at positive Z-scores, and we do not see a statistical edge to include some of them to our portfolio.

Over the past few months, most of you have noticed our increased activity in closed-end funds as the inflow of volatility finally shook them up and created various arbitrage, and directional, opportunities for active traders like us.

Currently, we are cautious when we choose our long positions as most of the closed-end funds which hold municipal bonds have lost their statistical edge and are traded at positive Z-scores. However, there are several interesting pair trade opportunities which can be traded. For the conservative market participants with longer investment horizon, I still see interesting dividend opportunities which are traded at high discounts.

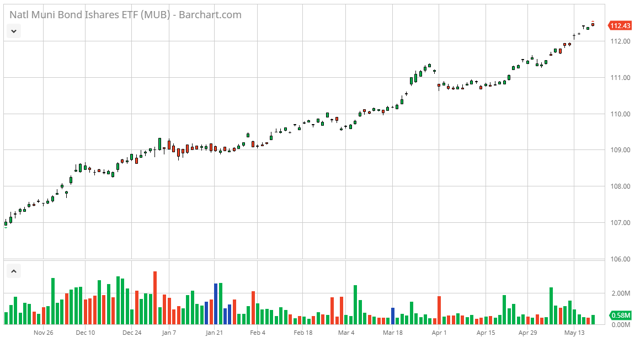

The benchmark of the municipal bonds iShares National Muni Bond ETF (

MUB

) reached new highest levels for the year after another positive performance. Over the past week, the main index increased its price by $0.54 and finished at $112.43 per share.

The recent volatility in the stock market and all of the events around the trade deal and its potential outcome continued to be a worrying factor for the market participants. As a result, we saw more demand for safer assets such as municipal bonds and closed-end funds which invest in them.

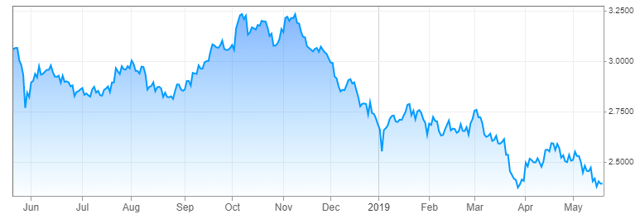

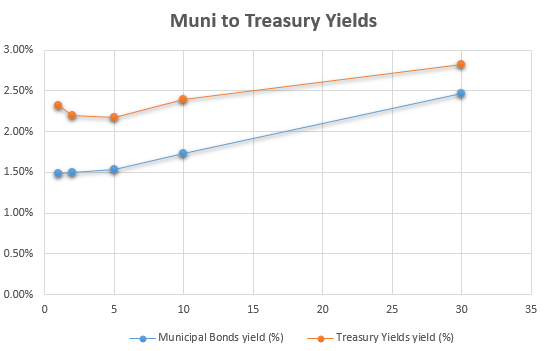

We also pay attention to the changes in the 10-year Treasury note. The municipal bond closed-end funds highly depend on its movements due to their relatively high duration. Currently, the 10-year Treasury yield is in a downtrend which is another stimulating factor for the municipal bonds.

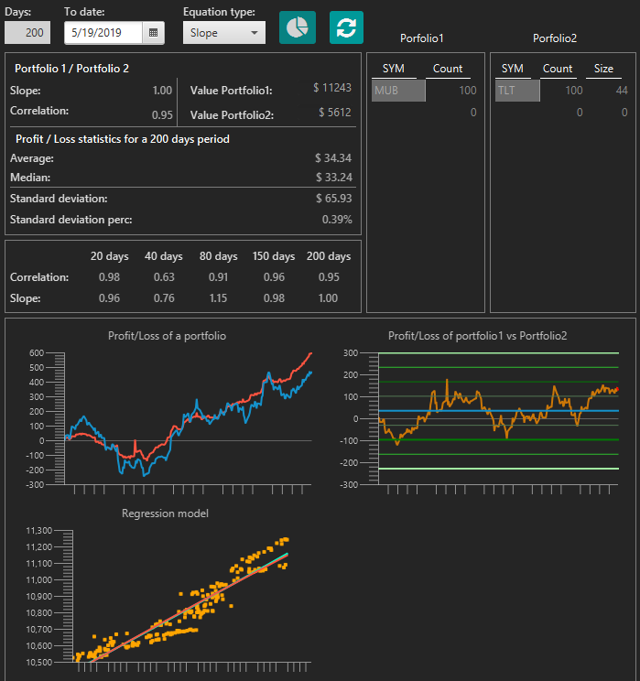

As you know, we follow the performance of the U.S. Treasury bonds - considering them a risk-free product - with maturities greater than 20 years: the iShares 20+ Year Treasury Bond ETF (

TLT

). The reason for that is the strong correlation between these major indices and the chart below proves it. Additionally, a statistical comparison is provided by our database software:

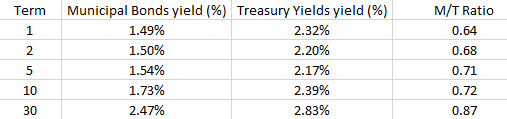

Investing in municipal bonds is popular because they have the potential to offer higher yields than similar taxable bonds. If an investor wants to know whether muni bonds are cheap in comparison to taxable bonds or Treasuries, they could find out by comparing them. However, this method does have its limitations, and the investor should perform a more thorough analysis before making a decision:

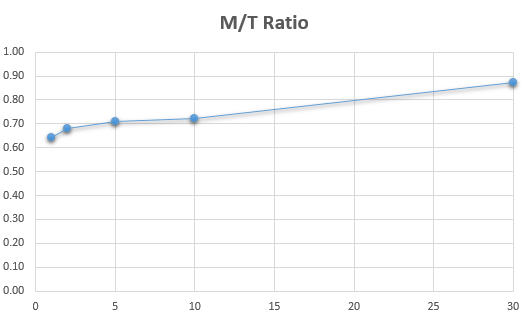

The Municipal/Treasury spread ratio or M/T ratio as it is more commonly known is a comparison of the current yield of municipal bonds to U.S. Treasuries. It aims to ascertain whether or not municipal bonds are an attractive buy in comparison. Essentially, an M/T ratio north of 1 means that investors receive the tax benefit of muni bonds for free, making them even more attractive for high net worth investors with higher tax rate considerations.

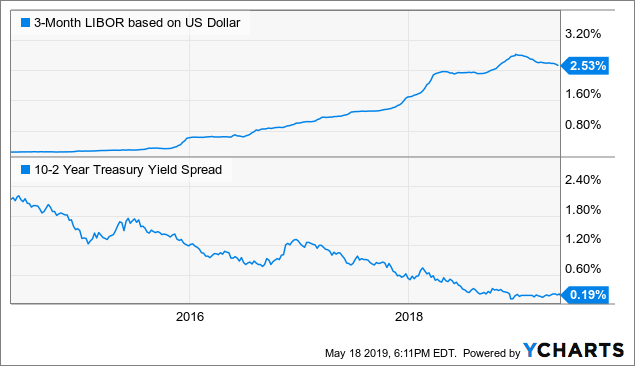

The narrowing spread and 3-month LIBOR are important for the leveraged municipal funds, and they can be highly affected by them. The 3-month LIBOR rate is a commonly used funding benchmark for the municipal bond CEFs.

Data by YCharts

Over the past week, several funds announced their regular dividends:

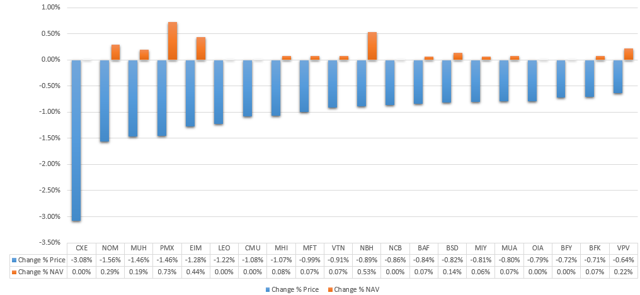

1. Biggest price decrease

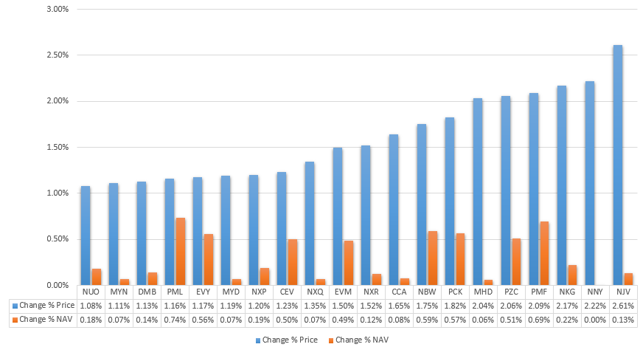

2. Biggest price increase

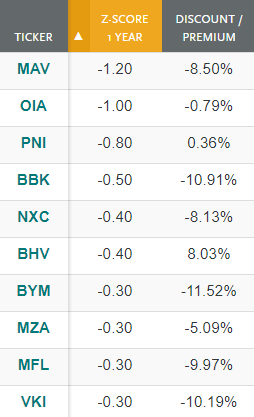

1. Lowest Z-Score

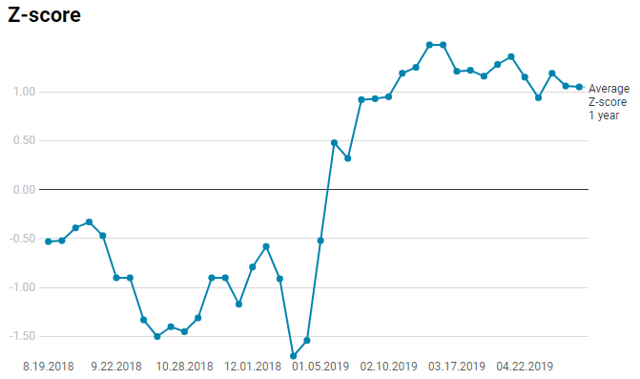

Above, I have plotted potential

"Buy"

candidates based on their Z-score. The purpose of this indicator is to show us how many times the discount/premium deviates from its mean for a specific period. Despite the positive week for the benchmark, the closed-end funds did not increase their Z-scores. To use appropriately the statistical edge, I try to combine it with an attractive discount in order to review some of the participants as potential

"Long"

candidate.

Currently, BlackRock Municipal Bond Trust (

BBK

) and BlackRock MuniYield Arizona Fund (

MZA

) are the funds which meet my requirements. I am not going to recommend all of the other funds. Even though, Invesco Advantage Municipal Income Trust II (

VKI

) and BlackRock MuniHoldings Investment Quality Fund (

MFL

) have attractive discounts and offer relatively high yields, you will notice the worrying situation about their earning/coverage ratios. In short, I think they will not be able to maintain the current dividend and pretty soon we may see dividend cuts. The market participants noticed it and this is one of the main reason why they are traded at negative Z-scores.

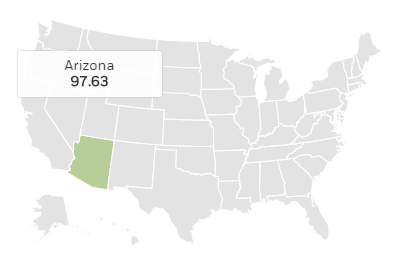

Based on the statistical approach, BlackRock MuniYield Arizona Fund is one of the most undervalued funds from the sector. Almost all of the assets from the portfolio of MZA are from issuers located in Arizona. "Education" and "Utility" sector have the biggest weight in the portfolio and the main part of the investments is labeled as "AA" and "A" ratings.

In December, the dividend was decreased from $0.0520 to $0.0470 per share. This is one of the main reasons why the price fell and the fund is currently trading at 5.09% discount. The current yield is 4.10% and the yield on net asset value is 3.89%.

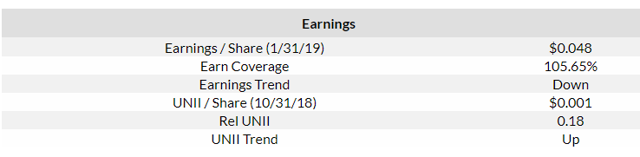

BlackRock Municipal Bond Trust has a current yield on the net asset value of 4.03%, and the current yield on price is 4.53%. Its Z-score of -0.50 point is accompanied by an attractive discount of 10.91%. Its earning/coverage ratio is 99.08%, but I still do not see a reason to worry about it. The fund has a positive UNII/Share balance of $0.048 per share which can be used.

2.

Highest Z-Score

On the other hand are the closed-end funds sorted by their highest Z-score. From a statistical point of view, they should be overpriced. In the current market environment when the sector is very strong, it is very difficult to say which of the Munis are overpriced. Yes, the Z-scores are high but they are still traded at discounts. My simple recommendation is to play the game smart and when some of your long positions are traded at Z-score above 2.00 points close it and buy some of the funds which have a lower statistical parameter. The risk/reward ratio is not in your favor when you hold statistically overpriced funds.

Last time, we saw BlackRock MuniYield Quality Investment Fund (

MFT

) on the first position with a Z-score of 2.80 points. I recommended you to close your long positions and to re-allocate your funds in some of its peers. The latest earnings of the funds are not enough high to cover the dividend, and if there is no improvement, we can expect dividend cut pretty soon. On a weekly basis, the price of MFT fell by 1.00% and it is among the worst performers of the weeks.

The average one-year Z-score in the sector is 1.05 points. Last time, the average Z-score of the municipal sector was 1.06 points.

3.

Biggest Discount

It is interesting to mention that only one of the municipal bond closed-end funds had a decrease in its net asset value on a weekly basis. The above funds are the ones with the highest spread between their price and net asset value. As we see, this sector still provides us with many closed-end funds traded at an attractive discount.

AllianceBernstein National Municipal Income Fund (

AFB

) is one of the funds which caught my eye. It is traded at 12.70% discount and has a relatively low Z-score of -0.10 point. The current yield of the fund is 4.21%, and based on the latest earnings report, we see that its dividend is fully covered. Based on the discount/premium metric, I find AFB as undervalued compared to its peers.

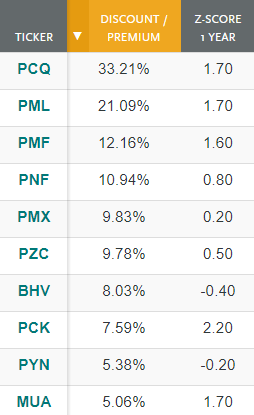

4.

Highest Premium

Although we recently saw dividend cuts for many of the PIMCO funds, they continue to be traded at high premiums. The trust in the management team and the good past results are one of the main reasons why the market participants want to have them even at a price higher than the net asset value. However, behind each investment and trade should be a justified reason and logic. My research shows that PIMCO California Municipal Income Fund (

PCQ

) may be a risky investment at that point of time due to the potential dividend cut which can be expected.

Also, if you have a long position in BlackRock MuniAssets Fund (

MUA

), I see the current period as favorable to close it and to select another good buying opportunity from the sector. My personal opinion is that it is overpriced compared to its peers, and its Z-score and premium are the confirming signals.

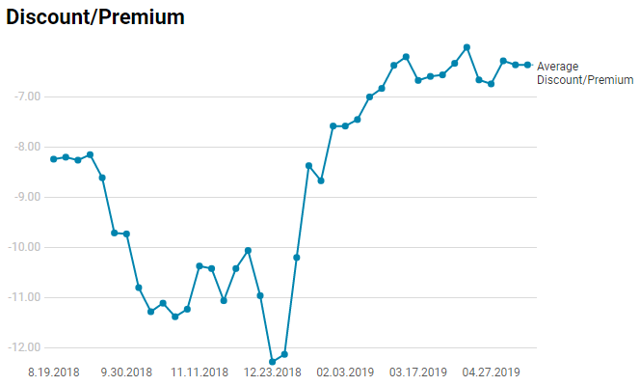

The average discount/premium of the sector is -6.36%. Last time, the average spread between the prices and net asset values of the funds was the same.

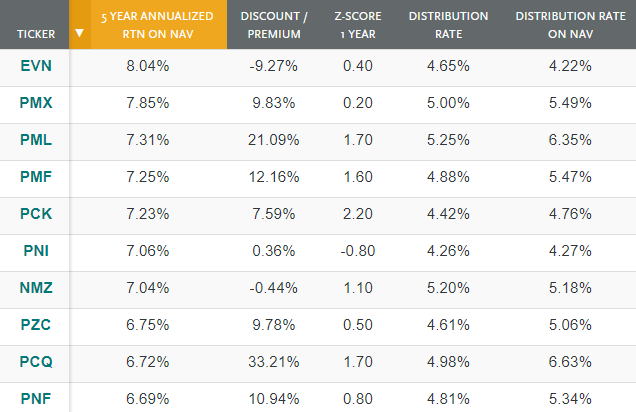

5. Highest

5-year Annualized Return On NAV

The above sample shows the funds which outperformed their peers. The average return on net asset value for the past five years for the sector is 5.07%.

I think PIMCO New York Municipal Income Fund II (

PNI

) deserves attention. PIMCO fund traded close to its net asset value, and at negative Z-score may be reviewed as potential

"Long"

candidate.

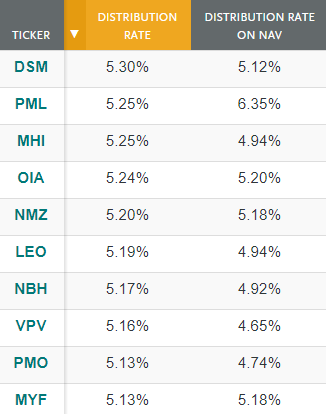

6.

Highest Distribution Rate

:

The table shows the funds with the highest distribution rate on price. The average yield on price is 4.42%, and the average yield on net asset value is 4.15%. An important notice which I would like to make here is to be rational and to include the earning/coverage ratio to your analysis. Some of the market participants invest in the funds which pay higher yields, but they do not take into consideration the risk of a potential dividend cut if the dividend is not covered by the earnings.

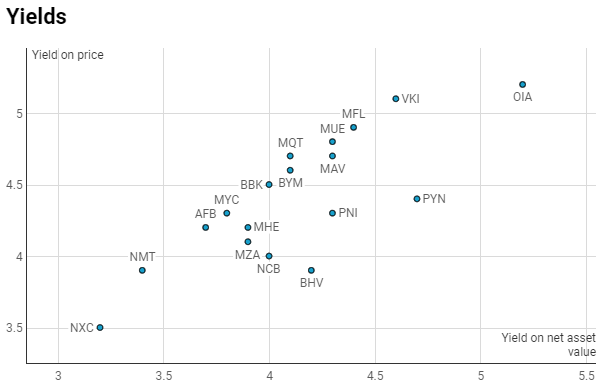

Below on the chart, I plotted the yields of funds from the sector which are traded at negative Z-score.

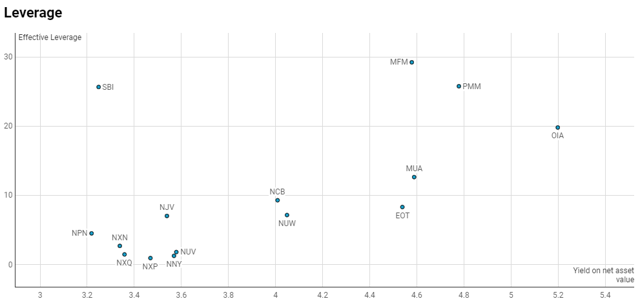

7.

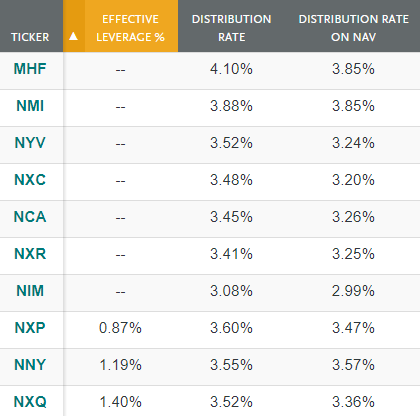

Lowest

Effective Leverage %

The average effective leverage of the sector is 36.2%. Logically, most of the funds with lower effective leverage have lower distribution rates compared to the rest of the closed-end funds. Seven funds from the sector have effective leverage equal to zero.

Below, you can find the chart of the funds with the lowest effective leverage and their yields on net asset value. If you are not a big fan of the high leverage, this chart will be very helpful.

Compared to the previous years, the discounts of the closed-end funds holding such products have significantly widened, but we remain cautious when we select our long positions due to the high Z-scores in the sector. However, there are several interesting pair trades which you can review.

I/we have no positions in any stocks mentioned, but may initiate a short position in PCQ over the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

推薦文章

美股前瞻 | 韓國KOSPI指數狂飆18%!SK海力士盤前再升逾6%;特朗普政府入股七家晶片公司;亞馬遜盤前勁升11%

一周財經日曆 | 7月大小非農重磅來襲;SpaceX迎首份財報+鉅額解禁,匯豐、閃迪、Palantir、AMD財報輪番登場

從「無人問津」到全球資金「新寵」!恆指月內飆升近13%,三路「活水」強勢匯入,港股還能強多久?

華盛早報 | 美股上演"AI大奇蹟日」!閃迪漲25%、美光漲18%;微軟暴漲15%創18年來最大漲幅;巨頭績后分化,亞馬遜大漲近10%,蘋果跌近6%

7月31日外盤頭條:亞馬遜雲業務營收大增37% OpenAI降價至多80%鞏固市場 蘋果iPhone銷量同比大漲22%

美股前瞻 | 聚焦20:30!沃什「欽點」核心PCE攜GDP數據齊登場;晶片股盤前強勢反攻,閃迪升近6%;蘋果、亞馬遜盤后放榜

全文|Meta Q2業績會實錄:消費級個人智能體最終市場會很廣闊

債市「用腳投票」:沃什鷹派言論難敵按兵不動,30年期美債收益率飆至19年新高