熱門資訊> 正文

Stablecoins — The New Era of Financial “Colonization” and the Last Bastion of Dollar Dominance

2025-07-18 02:51

TradingKey - On May 20, the U.S. Senate passed preliminary procedural votes on the “Guidance and Establishment of a National Stablecoin Innovation Act” (commonly known as the Stablecoin “Genius Act”).

This legislative momentum quickly reverberated across developed economies, with jurisdictions including Hong Kong, the UK, South Korea, and the European Union introducing their own stablecoin regulatory frameworks shortly thereafter.

Although the bill was subsequently rejected by the House of Representatives and sent back to the Senate for reconsideration on July 15, market observers view its eventual enactment as inevitable. Lawmakers from both major parties largely share a consensus on fostering the stablecoin industry’s development. Notably, U.S. Treasury Secretary Scott Bessent has voiced positive sentiments about stablecoins on multiple occasions, even publicly asserting that “cryptocurrencies do not pose a threat to the U.S. dollar, and stablecoins can reinforce the dollar’s global dominance.”

What Are Stablecoins?

Investors familiar with cryptocurrencies will undoubtedly recognize USDT (Tether) and USDC (USD Coin) as the two leading stablecoins by market share. But what exactly are stablecoins?

Essentially, stablecoins are blockchain-based cryptocurrencies designed for price stability, distinguishing them from more volatile assets like Bitcoin or Ethereum.

Taking Tether as an example: investors exchange U.S. dollars with Tether Limited — the issuer — on a 1:1 basis. Conversely, each issued unit of Tether must be backed by an equivalent dollar reserve held by the issuer. Investors can redeem a unit of Tether anytime at a one-dollar price point. This 100% reserve-backed guarantee, coupled with market arbitrage mechanisms, maintains Tether’s price peg effectively at $1.

Apart from price stability, stablecoins also offer two significant advantages over traditional fiat currencies: privacy and convenience.

Compared to traditional international payment systems — SWIFT, stablecoins leverage blockchain's distributed ledger technology to deliver superior transaction speed and lower costs. Cross-border payments with stablecoins can cost roughly one-tenth of SWIFT fees and settle dramatically faster — typically within five minutes versus the two to five days required for conventional cross-border settlements.

From a privacy standpoint, stablecoin transactions occur via blockchain wallet addresses without mandatory real-name verification, contrasting with traditional systems that require institutions to record the real identities of transaction parties. However, it is important to note that blockchain transactions are transparent and publicly accessible, meaning anyone with your wallet address can view transaction histories and details.

Finally, although current legislation strictly prohibits stablecoins from generating interest, many trading platforms are offering their own interest-bearing stablecoin deposit products to attract users. Leading exchanges such as Binance and OKX provide annualized interest rates around 5% for 90-day Tether deposits.

Why Issue Stablecoins?

The United States’ proactive push to develop stablecoins is driven by four core objectives:

Preserving Dollar Dominance

This goal is relatively straightforward. Years of lax fiscal discipline and the weaponization of the dollar have accelerated efforts toward “de-dollarization,” especially after the Russia-Ukraine conflict. Aggressive tariff policies under the Trump administration further constrained non-U.S. countries’ access to dollars.

Many central banks have been reducing their U.S. Treasury holdings in favor of gold and other sovereign debt to diversify reserves, directly challenging the dollar’s global dominance. As a result, the dollar index has steadily declined, while alternative assets like gold and Bitcoin have surged to record highs.

The introduction of stablecoins is expected to reinvigorate demand for dollar-denominated digital assets among non-U.S. countries, particularly emerging markets and developing economies. Citizens enduring volatile local currencies and domestic inflation naturally gravitate toward holding stablecoins. This trend is already widespread in countries such as Brazil, Argentina, and Venezuela.

Weakening the Federal Reserve’s Power

A significant divergence exists between the Federal Reserve ( Jerome Powell) and the White House (Trump) regarding interest rate policy. Historically, the Fed held a monopoly over money creation. While issuing stablecoins does not equate to minting new money — since stablecoins do not increase the money supply nor serve credit expansion — it allows issuers to absorb substantial amounts of U.S. dollars from the public and reinvest those funds in Treasuries.

This dynamic can influence short-term yields and undermine the Fed’s monetary policy transmission. Moreover, stablecoins operate outside the SWIFT network and fall beyond the Fed’s direct regulatory oversight.

Alleviating Short-Term Principal Repayment Pressure on U.S. Debt

The federal debt has ballooned close to 37 trillion, making interest payments the second−largest fiscal expenditure — exceeding even defense spending.

The recently enacted “OBBB” projected to add another 3.4 trillion in deficits over the next decade. Financial institutions holding Treasuries can issue corresponding stablecoins proportionally, using the deposits to buy more U.S. debt, thereby enabling risk-free arbitrage and on-chain recycling of Treasuries. This mechanism reduces the Treasury’s need to repay large principal amounts as bonds mature, allowing for continual rollover and limiting expenses to interest payments alone.

Data Sources: Treasury Government, TradingKey As of: May, 2025

Maintaining a Leading Position in the Global Crypto Market

Since the advent of cryptocurrencies such as Bitcoin and Tether, many nations have maintained a cautious regulatory stance due to concerns over decentralization and on-chain security. However, with technological advances and growing transaction volumes, most countries have gradually shifted from resistance to acceptance. The U.S., home to numerous leading crypto enterprises and technology talent, aims to integrate cryptocurrencies into its financial system. This strategy helps solidify and extend America’s monopoly in the global financial sector.

Is There Still Room to Participate in Stablecoins?

The concept of stablecoins has been around for some time, with transaction volumes skyrocketing in recent years. Data show that in the first half of 2025, stablecoins — led by Tether (USDT) and USD Coin (USDC) — processed around 6 trillion in transactions, with a full−year estimate of 12 trillion. Once the legislation passes, long-term conservative projections peg annual transaction volumes soaring to 40 trillion.

By comparison, the global SWIFT system processes roughly 8000 trillion annually, highlighting the immense growth potential for stablecoins. Moreover, blockchain technology is poised for further innovation. For instance, the burgeoning Real World Assets (RWA) sector — tokenizing tangible assets on-chain — promises more efficient, transparent, and cost-effective asset exchange and financing.

Although regulatory approaches to stablecoins vary significantly across countries, rapid legislative initiatives in the U.S., EU, Singapore, and others have laid a solid foundation for a new era of global currency transactions.

From the perspective of advantages and growth prospects, stablecoins indeed offer substantial appeal and opportunity. However, before diving in, investors should carefully consider several critical risks:

- Circumvention of Central Banks and Regulators: Stablecoins backed by the U.S. dollar and Treasury bonds can bypass national central banks and regulatory frameworks entirely. This undermines conventional monetary policy tools, potentially leaving economies, businesses, and consumers exposed to catastrophic fallout in the event of systemic financial crises.

- Issuer Credit Risk: Although stablecoins appear backed by U.S. dollar credit, the true guarantee rests with issuing entities rather than the U.S. Treasury. Issuers, like Tether Limited — which ranks as the fourth-largest holder of U.S. Treasuries — do not keep dollar reserves idle but actively invest them. Should liquidity strains trigger mass redemptions, stablecoins could precipitate a new systemic crisis.

- Cybersecurity Threats: Frequent hacker breaches have afflicted major crypto exchanges, including Binance, resulting in substantial direct losses. Network security remains a persistent vulnerability.

- Immature Regulatory Environment: Global regulatory frameworks for stablecoins remain nascent and fragmented. For example, in the U.S., stablecoin licensing authority can devolve to state governments, lacking cohesive federal oversight and uniform standards. Consequently, the regulatory landscape is patchy and uneven, facilitating uneven enforcement and potential abuses.

- Payment Adoption Challenges: Ultimately, U.S. policymakers envisage stablecoins as a new payment medium. Their widespread adoption hinges on offering unique advantages over traditional dollar transactions. Without compelling incentives, stablecoins will struggle to achieve broad market traction.

In summary, embracing U.S. dollar-backed stablecoins effectively means tying one’s assets to the stability of the U.S. financial system. As noted by Chair Rabbit’s incisive commentary: at its core, the U.S. stablecoin legislation leverages foreign monetary sovereignty ("fleecing") to provide breathing room for America’s fiscal irresponsibility and unsustainability — while simultaneously entrenching dollar hegemony by binding other economies to its system.

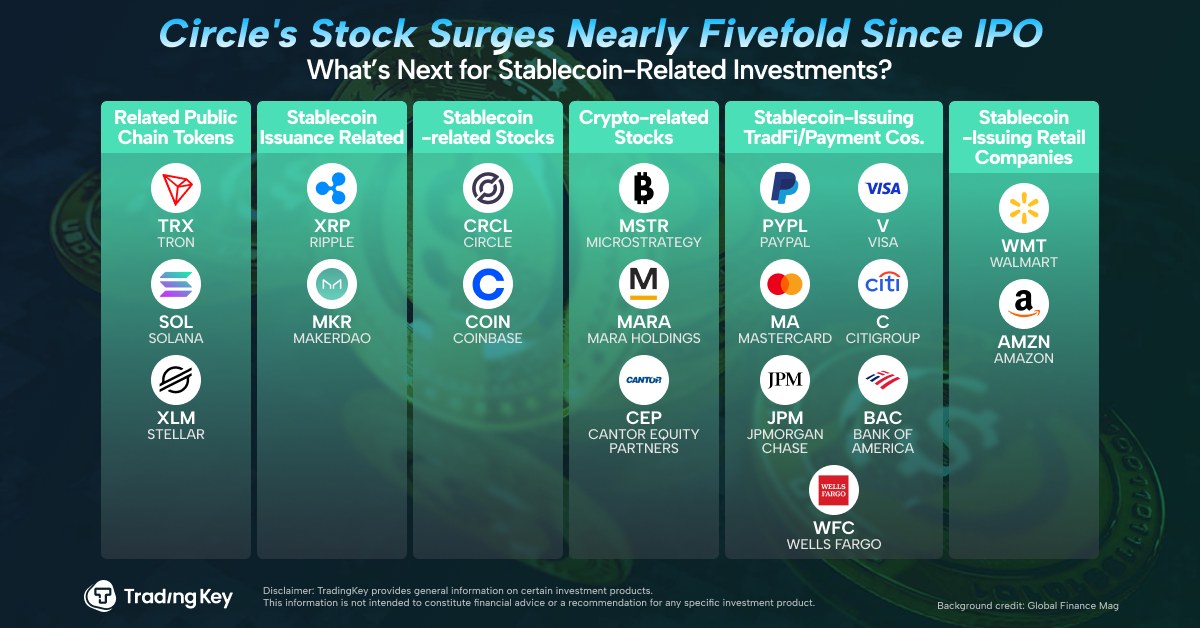

How Can Investors Gain Exposure to Stablecoins?

For investors looking to gain exposure to stablecoins and related sectors, direct participation through specific stocks and cryptocurrencies — outlined in the accompanying chart — is one option. Additionally, several ETFs provide targeted access to the broader crypto and digital economy space:

- Bitwise Crypto Industry Innovators ETF (BITQ)

- FT SkyBridge Crypto Industry & Digital Economy ETF (CRPT)

Both ETFs are among the earliest established products focused on crypto-related assets. While neither invests directly in stablecoins, they offer indirect exposure to the ecosystem. BITQ primarily concentrates its underlying holdings on core crypto infrastructure companies — such as mining firms, exchanges, and technology service providers.

In contrast, CRPT combines crypto assets with stakes in premium digital economy companies, including Nvidia and Meta Platforms. Due to these differences in portfolio composition, the two ETFs have exhibited noticeably divergent cumulative returns over the past three years, reflecting their distinct strategic focuses.

Data Sources: TradingKey As of: July 17, 2025

Data Sources: TradingView, TradingKey As of: July 17, 2025

推薦文章

美股機會日報 | 阿里發佈千問3.5!性能媲美Gemini 3;馬斯克稱Cybercab將於4月開始生產

港股周報 | 中國大模型「春節檔」打響!智譜周漲超138%;鉅虧超230億!美團周內重挫超10%

一周財經日曆 | 港美股迎「春節+總統日」雙假期!萬億零售巨頭沃爾瑪將發財報

一周IPO | 賺錢效應持續火熱!年內24只上市新股「0」破發;「圖模融合第一股」海致科技首日飆漲逾242%

從軟件到房地產,美國多板塊陷入AI恐慌拋售潮

Meta計劃為智能眼鏡添加人臉識別技術

危機四伏,市場卻似乎毫不在意

財報前瞻 | 英偉達Q4財報放榜在即!高盛、瑞銀預計將大超預期,兩大關鍵催化將帶來意外驚喜?