热门资讯> 正文

复盘巴菲特苹果持仓及相关评价最全总结

2021-05-08 10:22

- 伯克希尔(BRK.A) 0

- 苹果(AAPL) 0

- 伯克希尔B(BRK.B) 0

五一期间,我对巴菲特在苹果公司持仓和相关问答做了个小总结。主要是想了解下,他老人家是如何将苹果公司纳入他的能力圈的。先上一张总结图:

想到这个话题主要是因为,2020年,巴菲特在苹果公司上的持仓已经达到他整个投资组合的40%以上。在5月2日巴菲特股东大会的Q&A环节,一开始就有股东提出了这样的问题:

为何伯克希尔在2020年末卖出部分苹果公司股票,是否还继续看好苹果公司?

巴菲特的回应总结起来有几点:

Tim Cook很棒,他能做一些乔布斯做不到的事情(应该是指供应链管理方面)。

苹果产品的满意度超过99%,正在使用苹果手机的人很难转投其他阵营。

苹果手机的必要性可以媲美汽车(对美国人而言)。

2020年末卖出部分苹果公司股票,可能是一个错误。

不希望苹果公司受到反垄断法的影响。

如无意外,苹果公司还会继续成为巴菲特的第一重仓股。众所周知,巴菲特曾经多次说过自己不懂科技股,而苹果公司又是如何进入他的能力圈并成为他的最爱?我从持仓记录和股东大会问答中寻找到了一些蛛丝马迹。

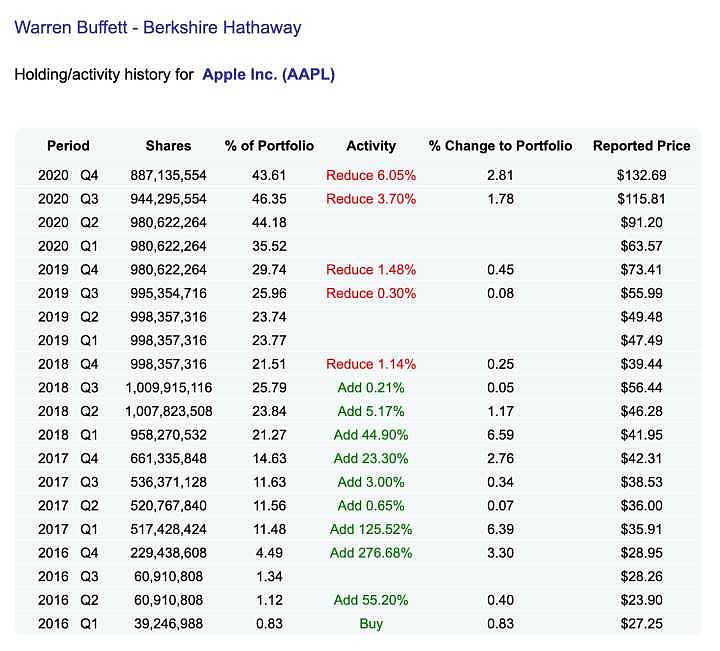

持仓记录:在2016-2018年间疯狂加仓

做什么比说什么更加重要。我先研究了巴菲特在苹果公司上的历史持仓情况(数据来源dataroma)

从持仓记录可以发现这样一些信息:

巴菲特从2016年开始投资苹果公司,在此此之前没有进行任何操作。

他在2016年底至2018年初期间进行了多次重大加仓,使得他在苹果公司上的持仓比例超过了整个组合的20%。

2018年Q4之后,巴菲特没有继续加仓苹果,反而卖出了少量股票(尤其是2020年Q4)。然而,得益于苹果公司股价的上涨,持仓比例不降反升,达到了2020年Q4的43.61%。

苹果拯救组合业绩

巴菲特近两年苹果公司持仓比例的上升,主要是股价上涨而非加仓的原因。根据这点推理,巴菲特应该减仓了一些股票(清空航空股),并且其他重仓股的表现也一般。

我对比了BRK最新五大持仓股票在2020年间的走势,仅有苹果一只股票大幅上涨。另外几只重仓股(BAC、KO、AXP和KHC)都有不同程度的下跌。

说一句苹果拯救了巴菲特的投资组合不为过。

在苹果的重仓程度是绝无仅有的

虽然巴菲特以集中持股著称,但这种单一股票仓位达到40%以上的情况还是绝无仅有的,甚至有点违背分散性原则。

我统计了过去十几年间巴菲特的第一重仓股在整个组合中的占比情况:

AAPL:2020Q3,最大持仓占比46.35%

KHC:2016Q3,最大持仓占比22.63%

WFC:2015Q2,最大持仓占比24.14%

KO:2010Q4,最大持仓占比25.03

除了苹果以外,单只股票重仓的极限在20%-25%之间,也难怪巴菲特加仓苹果达到25%后就没有继续加仓了。我猜想他可能会有25%的重仓占比上限(超过后就不加仓)。

股东大会Q&A:将苹果纳入能力圈

接下来,我尝试从另外一条线索(股东大会Q&A)入手。看看随着时间的变化,巴菲特对苹果公司的评论有什么变化。

从1994年开始,巴菲特在股东大会上会回答各种千奇百怪的问题,其中就有一些是关于苹果公司的。经过漫长的数据清洗后,我从中捞出了十几条有关苹果公司的Q&A(这可能是全网巴菲特对苹果评价的最全总结):

有意思的是,这些Q&A基本能够和持仓记录对应上,也可以大致分为三个阶段:

2016年以前(观望期):苹果公司是好公司,但是没把握

2016年-2018年(加仓期):苹果公司是巴菲特持续学习的标志

2019至今(稳定持有期):苹果公司股价涨得太快,没法加仓

以下是所有的相关问答。我将段落进行了摘抄和简要翻译,并附上英文原文以供参考。

2016年以前(观望期):苹果公司是好公司,但是没把握

2010年:巴菲特没有在股东大会中提及过苹果公司(有点震惊),直到2010年的股东大会,巴菲特在回答“什么样的公司能够带来最棒的资本回报率”时,他才正面表扬了苹果公司的商业模式。

苹果这样的轻资产优质公司,不需要太多资金。最好的商业模式是能够做得很大并且没有太多资金需要的。

But there are a lot of great businesses that need very, very little capital. Apple doesn’t need that much capital, you know.

The best ones, of course, are the ones that can get very large while needing no capital.

2012年:在回答“你们已经投资了IBM,为什么不考虑谷歌或者苹果”(当时IBM是伯克希尔的重仓股之一)时,巴菲特说,相比谷歌/苹果,他在IBM上的把握更大。

对我们而言,在IBM上犯错的几率比在谷歌或者苹果上更小。但这并不是说,谷歌或者苹果不会在将来比IBM发展更好。

我无法预测到苹果过去十年的发展轨迹,我也很难想象苹果的下一个十年会发生什么。

The chances of being way wrong in IBM are probably less, at least for us, than being way wrong with Google or Apple. But that doesn’t mean that those — the latter two companies —aren’t going to do, say, far better than IBM.

But we wouldn’t have predicted what would happen with Apple 10 years ago. And it’s very hard for me to predict, you know, what will happen in the next 10 years.

2013年:在问题“能否提供一些分析股票的量化指标”中,巴菲特说对苹果没有足够的把握。

我们知道Burlington Northern铁路公司肯定会通过电子系统提升效率,保持15年的竞争优势。但我们对苹果没有这样的把握,不管苹果的财务报表多么的光鲜亮丽。

We think that the Burlington Northern will have a computer — a competitive —advantage 15 years from now, with a high degree of confidence. We would never have that degree of confidence about Apple, no matter what their financial statement showed.

2016年-2018年(加仓期):苹果公司是巴菲特持续学习的标志

2016年:巴菲特在回答企业融资相关问题时,提到苹果公司会通过供应商进行融资(应该是将资金压力转到供应商上)。

像苹果或戴尔这样的公司会通过供应商进行融资,所以他们的营运资金可以是负的。

It has become increasingly common for companies like Apple and Dell to finance their business via their suppliers, in some cases with negative working capital.

2017年:由于13F披露了巴菲特在2016年开始投资苹果公司的信息,所以有多条相关问答。在回答“你近些年学习到的最有意思的事情”时,芒格提及苹果公司是巴菲特持续学习的标志。

芒格:购买苹果股票是巴菲特持续学习的标志。

CHARLIE MUNGER: Well, I think buying the Apple stock is a good sign in Warren. (Laughter)

在回答“你为何开始投资科技公司”时,巴菲特说他更愿意将苹果公司看作一家消费品公司。

我们是在苹果公司上持有很多股票,但我更愿意将苹果看作一家消费品公司(而不是科技公司)。

And, then, fairly recently, we took a large position in Apple, which I do regard as more a consumer goods company, in terms of certain economic characteristics.

在回答“伯克希尔是否更应该投资轻资产公司”时,芒格比较了化学品公司和苹果/谷歌,并说道后者才是目前正确的商业趋势。

芒格:美国的化学品公司曾经是非常棒的投资选择。陶氏化学(Dow)和杜邦(DuPont)曾经的市盈率是20倍左右,他们持续开发新的化学品,请更多的专业人才。他们是那个时代明星。

如今,大部分化学品都沦为难以差异化的日用品(Commoditized),而化学品行业的竞争也很激烈。现在是苹果或者谷歌的时代。

我觉得提问者基本上是对的。如今的商业世界变化很大,选择苹果/谷歌这样新的商业领域比旧领域(化学品行业)要成功得多。

CHARLIE MUNGER: Yeah. The chemical companies of America, at one time, were wonderful investments.

Dow and DuPont sold at 20-some times earnings, and they kept building more and more complicated plants and hiring more Ph.D. chemists, and it looked like they owned the world. Now, most chemical products are sort of commoditized and it’s a tough business being a big chemical producer. And in comes all these other people like Apple and Google and they’re just on top of the world.

I think the questioner’s basically right that the world has changed a lot, and that the people who have made the right decisions in getting into these new businesses that are so different from the old ones have done very well.

在回答“你从投资IBM这样的科技公司中学到了什么(教训)”时,巴菲特说苹果和IBM是完全不同的公司。

巴菲特:我将IBM和苹果视为两家不同的公司。虽然我在六年前买了IBM,并且那时认为IBM会表现得更好。

而苹果,我觉得很不一样。我觉得苹果更应该被视为一家消费品公司,如果你分析它的护城河以及消费者的行为(对苹果产品的忠诚),你就会明白。

WARREN BUFFETT: Well, I do view them differently. But, you know, obviously, when I bought the IBM — started buying it six years ago — I thought it would do better in the six years that have elapsed than it has.

And Apple — I regard them as being in quite different businesses. I think Apple is much more of a consumer products business, in terms of the — in terms of sort of analyzing moats around it, and consumer behavior, and all that sort of thing.

2018年:巴菲特关于苹果公司有了更多分析,有四个相关问答。在回答“是否会考虑除苹果外的其他科技公司,比如亚马逊和谷歌”时,巴菲特说他投资苹果是在分析了苹果生态系统的价值、这个生态系统能持续多久、有什么潜在威胁这一系列问题后作出的决策。

我们肯定会考虑其他科技公司。我们并不是抱着“我们是不是应该买多一些科技股”的心态去投资的,而是去思考这家公司是否有持续的竞争优势,以及我们对这家公司的认知是否会超过其他投资者。

...

我并不是因为苹果公司是一家科技公司而去投资它的。我投资苹果是在分析了苹果生态系统的价值、这个生态系统能持续多久、有什么潜在威胁这一系列问题后作出的决策。

我也不觉得这样的分析需要我将iphone拆解,搞清楚它的各个部件才能进行。这其中更多的是消费者行为和心理的分析。

Well, we certainly looked at them. And we don’t think of whether we should be in tech companies or not, or that sort of thing. We are looking for things when we do get into the durability of the competitive advantage, and whether we think that our opinion might be better than other people’s opinion in assessing the probability of the durability, so to speak. ...

And I didn’t go into Apple because it was a tech stock in the least. I mean, I went into Apple because I made certain - came to certain conclusions about both the intelligence with which the capital would be employed, but more important, about the value of an ecosystem and how permanent that ecosystem could be, and what the threats were to it, and a whole bunch of things.

And that didn’t - I don’t think that required me to, you know, take apart an iPhone or something and figure out what all the components were or anything. It’s much more the nature of consumer behavior. And some things strike me as having a lot more permanence than others.

在回答“你如何预测某个产品将来是否会成功”时,巴菲特觉得iphone和喜诗糖果类似,都能给人带来美好的感觉。

关于喜诗糖果,设想如果你是一个加州男孩,你带着一盒喜诗糖果去女朋友家,然后她会回赠给你一个吻。所以你对喜诗糖果的价格并没有那么敏感。

所以我们真正需要的是,能够给我们带来美好感觉的产品(就像亲吻一样)。

而我们确实在以iphone为首的苹果生态系统上下了重注。我们在这种生态系统上看到了这种不一样的、给人带来美好感觉的特点。不过也许我是错的。

You know, you have to look at - See’s Candy, you know, if you live in California and you were a teenage boy, and you went to your girlfriend’s house and you gave the box of candy to her or to her mother or father and she kissed you, you know, you lose price sensitivity at that point. (Laughter)

So we really want products where people feel like kissing you, you know - (laughs) - rather than slapping you.

It’s an interesting thing. I mean, you know, in effect we’re betting on the ecosystem of Apple products, but - led by the iPhone. And I see characteristics in that that make me think that it’s extraordinary. But I may be wrong.

在回答“你为什么要投资重资产公司(铁路公司)”时,巴菲特说买苹果公司需要花很多钱。

像苹果这样的商业模式不需要太多资金。 但问题是,这种公司,你需要花很多钱去买,并且这样的机会并不多。

Yeah. And a business like Apple really doesn’t take much capital. But - so, you’ve got to spend a lot of money to buy businesses like that. Very few are for sale.

在回答“你是如何看待苹果的回购计划”时,巴菲特表示赞同,并且说回购计划可以增加伯克希尔在苹果公司的股权占比。

苹果有一些非常棒的电子消费品。如果觉得目前股价偏低,是可以回购。

...

我很乐意见到,苹果的回购计划让我们在苹果公司上的股权占比变得更多(在什么都不做的情况下)。 不过,苹果需要推出非常特别的产品(iphone),能够创造一个生态系统并且保持很高的客户黏性。

Apple has an incredible consumer product which you understand a lot better than I do. Whether they should buy in their shares - they shouldn’t buy in their shares at all, unless they think that they’re selling for less than they’re worth.

...

I find that if you’ve got an extraordinary product, and ecosystem, and there’s lots to be done, I love the idea of having our 5 percent, or whatever it may be, grow to 6 or 7 percent without us laying out a dime. I mean, it’s worked for us in many other situations.

But you have to have some very, very, very special product, and - which has an enormous wide - enormously widespread ecosystem, and the product’s extremely sticky, and all of that sort of thing.

2019至今(稳定持有期):苹果公司股价涨得太快,没法加仓

2019年之后,巴菲特没有继续加仓苹果,相关问答也变少了。2019年股东大会上仅有两个相关问题,2020年大家的注意力都在航空股上,甚至整个股东大会都没有提及苹果。

在回答“如何看待现在的信用卡市场和美国运通公司”时,巴菲特表示苹果也是竞争对手之一 (芒格甚至还提到了Wechat)。

苹果现在也是运通卡的竞争对手,他们与高盛合作推出了一种信用卡。

我认为信用卡市场会有很多竞争者。银行肯定不会放弃这块蛋糕,这是持续增长的领域。信用卡市场并不是赢家通吃的市场,各个玩家都会有一定的市场份额。

Yeah, everybody’s a competitor, including now Apple. It has just instituted a card, I guess, in conjunction with Goldman Sachs.

Everybody — there will always be, in my view, many, many competitors in the business. Banks can’t afford to leave the field. It’s a growing field. They build up receivables on it.

But I wouldn’t think of the credit card business as a one-model business any more than I would think of the car business as essentially being one model. I mean, Ferrari is going to make a lot of money, but they’re going to have just a portion of the market.

在回答“如何看待反垄断诉讼对苹果的影响”时,巴菲特表示苹果的问题是涨的太快,没法加仓。

我对苹果保持乐观,但感到遗憾的是:苹果的股价涨的太快了。我没办法加仓了。

芒格:我的家人都在使用iphone,并已经到了难以割舍的地步。

Well, again, I will tell you that all of the points you’ve made I’m aware of, and I like our Apple holdings very much. I mean, it is our largest holdings.

And actually, what hurts, in the case of Apple, is that the stock has gone up. You know, we’d much rather have the stock — and I’m not proposing anything be done about it — but we’d much rather have the stock at a lower price so we could buy more stock.

...

CHARLIE MUNGER: Well, in my family, the people who have Apple phones, it’s the last thing they’ll give up. (Laughter)

然后就是开头我提到的2021年的问答。

结束语

五一期间,我刷到了一些关于巴菲特的负面文章。我想说的是,很多人并不真正了解巴菲特。不知道这些打嘴炮的人有多少是真真正正看过他写的原文,听过他在股东大会上讲的话。

我尽可能客观描述我找到的一些证据。希望这篇文章,能够真实还原这位价值投资大师的学习过程

风险及免责提示:以上内容仅代表作者的个人立场和观点,不代表华盛的任何立场,华盛亦无法证实上述内容的真实性、准确性和原创性。投资者在做出任何投资决定前,应结合自身情况,考虑投资产品的风险。必要时,请咨询专业投资顾问的意见。华盛不提供任何投资建议,对此亦不做任何承诺和保证。

推荐文章

不止迈威尔科技!黄仁勋点名超30只“AI工厂”产业链公司,年内最高已抢跑480%涨幅

6月金股一图睇完 | 腾讯领衔“科网老登”集体反弹?科指月内累涨4%,机构称AI仍为核心增长引擎!

华盛早报 | 光通信利好连发!国产技术重要突破 + 迈威尔引爆美股+ 英伟达硅光量产;微软联手英伟达重新发明电脑;SpaceX拟定价135美元

6月3日外盘头条:特朗普签署AI行政令加强政府监管 微软发布全新AI模型 SpaceX要求压低IPO承销费率

港股盘中持续拉升!恒指涨超1.4%,科指涨超3.5%;美团绩后涨超8%,腾讯涨超7%,比亚迪股份涨逾5%

华盛早报 | 英伟达杀入PC芯片引爆产业链,ARM涨近16%;谷歌拟筹800亿美元押注AI!伯克希尔重金入局;美团环比大幅减亏超百亿

一图看懂 | 外卖大战趋缓!美团Q1调后净亏49.7亿,环比大幅减亏超百亿;管理层称补贴将更审慎

华盛早报 | 今天11点!黄仁勋发表重磅演讲,即将携手微软发布新款PC?马斯克辟谣SpaceX估值下调;美团盘后放榜