热门资讯> 正文

DocuSign: Impressive Quarter, But Valuation Now Expensive

2019-09-27 23:08

DocuSign reported a very strong quarter with revenue growing 41% and billings growing 47%, both well above consensus expectations.\n

Management raised full year revenue and billings higher than the Q2 beat, implying there could be continued strength during the rest of the year.\n

With the stock up over 40% since reporting earnings, valuation has expanded quite a bit, now ~11.6x forward revenue.\n

DocuSign (DOCU) reported a much needed strong Q2 earnings with their shares initially popping over 20% the following day. Since reporting earnings, their stock has been up over 40% and is now inching closer to their all-time highs. The stock has rebounded nicely after a strong quarterly report which saw upside to both revenue and billings in addition to management confidently raising their guidance.

Revenue grew 41% and billings grew 47%, both ahead of consensus expectations and management’s guidance range. The significant beat in billings growth was the main reason why the stock has been up, though management’s raised full year guidance also brought increased confidence to the investment community.

While the company seems to be running full steam ahead, so does their valuation. It was not too long ago where the stock traded near 9x forward revenue. Although revenue growth beat expectations, valuation has expanded quite a bit to ~11.6x FY20 revenue. At these levels, it is somewhat challenging to build a position in the name. I would wait until the stock reaches a plateau or self-corrects. Over the long-term, I am very bullish and believe investors will be rewarded appropriately.

DOCU held their analyst day a few months ago where they went through a potential $25 billion TAM opportunity with DOCU being the leading online player. Management's guidance calls for revenue of just under $1 billion during the year, meaning the company only has ~4% share of the TAM, which leaves a lot of room left for the company to grow.

The company is also in a wide range of different industries and verticals as their software solution is relatively standard. There is no need to greatly customize the service, which makes it easier for DOCU to move across a variety of verticals with ease. The company also as a great opportunity to expand internationally with less than 20% of revenue mix is international. As DOCU further penetrates into the domestic market and the global economy continues to encourage international business, DOCU has a significant opportunity to expand their presence internationally.

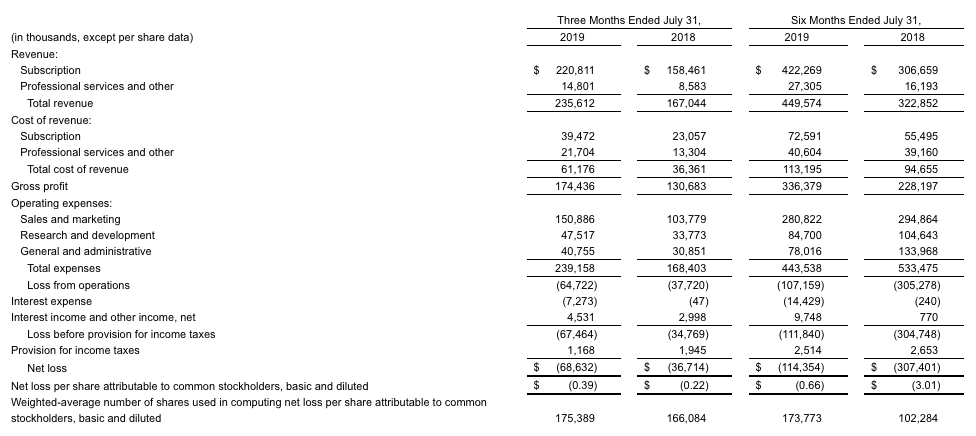

During Q2, revenue grew 41% to $236 million, which was above consensus expectations for 32% growth and ahead of management’s guidance range of $218-222 million. Revenue growth during the quarter also accelerated from the 37% growth in Q1, an impressive feat for a company running at a ~$1 billion run-rate.

Subscription revenue continues to drive the company’s growth, growing 39% during the quarter and represents ~95% of total revenue. Professional services revenue growth continues to remain healthy, however, subscription revenue is much more recurring in nature and has greater visibility into future revenue streams. This revenue continues to dominate the mix and investors are willing to place a higher multiple on subscription revenue compared to professional services revenue.

Billings grew 47% to $252 million and came in significantly above consensus expectations for $221 million and beat management’s guidance by ~$32 million at the midpoint. Billings growth was strong due to both domestic and international markets, demonstrating the company’s ability to grow their geographic footprint.

Gross margins continue to remain strong at 78%, despite being down slightly from 81% in the year ago period. Operating margin was a little weak during the quarter, coming in at roughly 0%, slightly worse than ~3% in the year ago period. G&A expenses were a little higher compared to the year ago period, but a majority of the lower operating margins stemmed from lower gross margins.

Despite the strong revenue beat, EPS during the quarter came in at $0.01, which was below consensus expectations of $0.04, though was somewhat non-important given the strong rebound and magnitude of beat in billings.

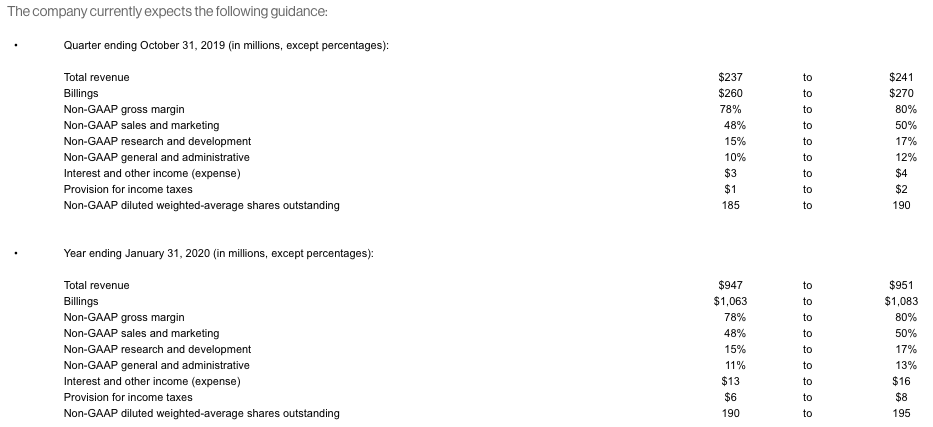

Management provided guidance for Q3 which includes revenue of $237-241 million. Billings are expected to be $260-270 million, which was ~$10 million higher at the midpoint than consensus expectations. Gross margins are expected to remain strong at 78-80% with operating margin of ~3% at the midpoint.

For the full year, management raised their expectations which helped lead to the stock’s strong performance over recent weeks. Revenue is now expected to be $947-951 million (up from $917-922 million) and compared to last year’s revenue of $701 million. Billings are expected to be $1.063-1.083 billion (up from $1.01-1.03 billion) with the ~$52 million raise well above the ~$32 million billings beat during the quarter.

Valuation has been challenging to determine given the company’s very strong revenue growth, though somewhat uneven billings growth. Last quarter we saw the stock pull back quite a bit as billings growth missed expectations. While growth metrics remain near the upper end of software companies, the stock has been punished due to occasional decelerating growth.

However, after the strong Q2 revenue and billings beat, investors felt very confident in management’s raised guidance, leading to the stock rising over 40% during the past few weeks. The stock currently sits near all-time highs and valuation has expanded quite meaningfully as well.

While there are several companies trading at higher forward revenue multiples than DOCU, I am not advocating for a re-rating higher. I think these names are good depictions on the upper-end of revenue valuation metrics. Investors recently saw Zscaler’s (ZS) multiple contract quite a bit after providing lower than expected guidance and profitability. This is an example on how these premium-valued companies can trade once investors sniff out deceleration.

DOCU currently has a market cap ~$11.35 billion and with ~$750 million of cash/investments and debt of ~$450 million, the company has a current enterprise value of ~$11.05 billion. Using management’s recently raised revenue guidance of $947-951 million, this implies a FY20 revenue multiple of ~11.6x.

Assuming the best-case scenario of management’s guidance being very conservative and FY20 revenue comes in at $1 billion (Q2 revenue just beat by ~$16 million), this would still result in a ~11x FY20 revenue multiple. Management’s current guidance implies FY20 growth of ~35% and assuming growth decelerates a little bit to ~32-33% during FY21, we could see FY21 revenue of ~$1.25 billion. Even at these levels, the stock trades at a somewhat expensive 8.8x multiple.

After the recent strong 40% performance in the stock over the past few weeks, valuation has reached a point where a lot of bullish outcomes have been priced into the name already. With the stock near all-time highs, I would be cautious around building a new position in the name and would wait for a pullback to add. Over the long-term, the company is poised to succeed, though valuation is a bit too much to handle right now.

Some risks to DOCU include competition from larger players, such as Adobe (ADBE). Also, companies with high revenue valuations tend to trade in a more volatile fashion if the company demonstrates slower revenue growth or misses consensus expectations.

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

推荐文章

美股前瞻 | 特朗普称美伊会谈明天召开!纳指期货升逾1%;太空概念股RKLB大涨12%,豪掷80亿美元收购铱星通讯;康卡斯特飙升22%

新股申购 | 6只新股今启招股!基本半导体一手入场费6387.78港元,中国自动驾驶公司MOMENTA-W一手入场费5971.62港元

华盛早报 | 三星、海力士预告1.3万亿美元大规模投资!中国存储重磅利好,苹果寻求购买长鑫存储芯片

iPad、Xbox接连涨价 折射出存储芯片短缺之痛

港股周报 | 阿里巴巴单周重挫15%!一众科网股继续“寻底”;南方两倍做多海力士ETF规模一度超盈富基金

一周IPO | “万元肉签”新股扎堆!下周还有8只新股上市;SK海力士拟以166美元IPO价登陆美股

美股前瞻 | 纳指期货盘前跌超1%,存储概念回调!SpaceX、CoreWeave获纳入获纳入罗素指数;花旗称AI交易仍未终结

一周财经日历 | 美伊谈判6月28日重启;6月大小非农数据重磅来袭;来福谐波、鲟龙科技等8只新股下周上市

{kind=link}

{kind=link}

{kind=link}

{kind=link}