热门资讯> 正文

担保看涨策略可能会在未来几年超越市场

2019-08-22 21:54

Over the last 10 years, covered call strategies have underperformed the S&P 500.

Covered call strategies only outperform the market in troubled times, like one could expect are coming up in the coming years.

The strategy provides investors with a few advantages.

More volatile stocks do not need to be sold off, as they will earn the investor a higher call premium.

The strategy can easily generate 2.5% cash inflow on a monthly basis, which could come in handy during market downturns.

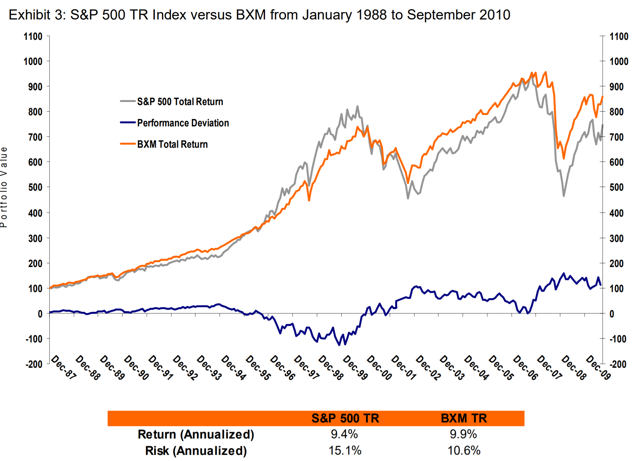

During the period 1987- 2009, a strategy of buying the S&P500 index while at the same time selling 1 month-ATM call on it, tracked by BXM (BXMX), outperformed the market by 70 basis points a year. This while only having two-thirds of the market's volatility. You can see the results for yourself in the following graph, the covered-call strategy is in orange:

However, since 2010, the strategy has underperformed the market. And quite drastically (covered call is in orange, SPY in grey):

This is simply because since 2010, there has not been a market drop large enough for the Covered-Call strategy to catch up with the SPY. One of the characteristics of assets with low volatility, is that they tend to go down less than other, higher volatility, assets. As the S&P is in a bull run since 2010, the covered call strategy has underperformed the broad market.

However, things might be about to change.

(pardon my language) IPO's, inverse yield curves, a looming trade war, negative growth of some big economies, Brexit, Italian banks... Several elements are pointing to an end of the bull market, or at least to a lot of volatility being on its way.

Let's compare the results of our covered-call strategy with the S&P500 during the last two crises (2001 and 2008):

While you would have lost around 12% with the covered index writing strategy over 2-2002, your losses would have been far bigger if you would have had just invested in the S&P 500, at around -40%...

The same goes for the financial crisis in 2008. You would have

gained

1.54% over the period from the first of January 2008 to the first of January 2010 with covered index writing. At the same time, you would have lost more than 16.5% if you had just invested in the S&P 500.

Now, it might be exactly the right time to switch to a covered-call strategy, as it bears only two-thirds of volatility and suffers less from a possible market downturn.

Most fundamentally, it is still about stock picking. I will not go too deep into this section as it is out of the scope of this article, but try to pick stocks you believe will beat the market over the coming years. However, it is important that you buy stocks that fit two criteria: 1. you can trade options on the stock; 2. you are willing to keep the stock for a long time; and potentially 3. the stock yields at least a small dividend, which cashflow allows you to buy back a written call if you don't feel like having your stock called. The risk of the stock (volatility, beta) is less important than in a normal buy-and-hold portfolio. I will come back to this.

The volatility of a stock determines the time value of an option on that stock, if the stock price does not change until maturity, the time value is the net profit you will have made. The higher the volatility, the higher the time value, but also the higher your risk.

The risk consists out of two possibilities: 1. the risk that the stock drops. If the drop is larger than the call premium you have received for that period, you make a net loss; 2. the risk that the stock goes up more than the strike price. In this case, you will get your stock called. However, you will make a profit in this case, as you pocket both the call premium and the capped profit on the stock.

The higher the volatility, the higher the chance that one of both possibilities occurs. By far, a drop that is not covered by the call premium is the worst-case-scenario. I will write in my follow-up article how one could minimize this risk.

In theory, the call premium (time value) should go up proportionally with the volatility of the stock. However, in practice, we see that the premium often is a tad bit higher than it theoretically should be.

In short, writing calls on high-volatility stocks brings along more risk, but is also rewarded better. This is the reason why you can still keep the high-volatility stocks in your portfolio, even now volatile times are coming: you are rewarded for them via the higher call premiums.

As you might have spotted in the picture above, the current stock price of Aperam (OTC:APEMY) (OTC:APMSF) is 20.49 euros. Its volatility is at 37.3% on a yearly basis. If we sell a call option with a strike price of 5% above the current stock price, at 21.50, we receive a premium of 0.46-0.55 euros. This is around a whopping 2.5%!

For Royal Dutch Shell, the volatility stands at 23%. Here, selling an option 5% above the current spot price returns at least 0.92%. Low-volatility stocks, with 15% volatility for example, "only" return 0.3% per month.

These earnings have two advantages:

1. A drop in the share price hurts less and can even be neutralized

For example, if Aperam drops 10% in a month, your net loss will be at around 7.5%. Furthermore, you can then write another call option, for 5% higher. This will pocket you another 2.5%. If the stock goes back up by more than 5%, it gets called and you are at break-even, while the stock can still be down by as much as 5%.

2. You are provided with a monthly cash-injection

When markets tumble, buying stocks on the cheap is a guarantee for long-term success. However, you need to have the cash to be able to do so. Writing calls can provide you with a monthly 0.5%-2.5% cash injection, which could come in very handy during such distressing times.

While covered call strategy most likely underperformed the S&P 500 over the last 10 years, it is set to beat the market over the coming years. It has beaten the S&P in both the last two market crashes and suffers way less from volatility. At the same time, it gives investors the possibility to keep volatile stocks in their portfolio, as writing calls 5% above the spot price generates a monthly return of 2.5%.

I am/we are long APEMY, RDS.A.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

推荐文章

美股机会日报 | 特朗普13日开启访华,据传"800人代表团"中会有谁?10000点!小摩再度上调韩国Kospi指数目标,还有33%上涨空间

腾讯、阿里等中概巨头业绩来袭!AI收入转化率成关键,这轮财报季能否助力恒科“反弹”?

华盛早报 | “完全不可接受”!特朗普拒绝伊朗方案,油价应声涨逾3%;中美将于明日在韩举行经贸磋商

港股周报 | 存储芯片持续飙升!两倍做多海力士周内狂涨64%;段永平重大调仓!清仓中国神华,大幅买入泡泡玛特

一周IPO | 4月“零破发”!5月更嗨?天星医疗首战暴涨118%;机器人扎堆!乐动机器人暗盘大涨近90%,翼菲科技火热招股中

一周财经日历 | 下周重磅大事齐袭!特朗普政府或携黄仁勋访华;中概科网股财报季打响!腾讯、阿里同日放榜

美股机会日报 | “TACO”已经过时?华尔街疯狂涌入“NACHO”交易;今晚20:30!美国4月非农或创年内最大落差?

马斯克再下注:SpaceX IPO倒计时 拟投1190亿美元建Terafab芯片厂