热门资讯> 正文

Circle Q2盈利洞察:其长期增长路径清晰吗?

2025-08-22 09:17

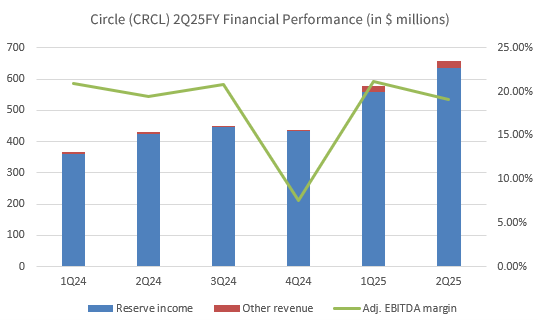

TradingKey - Circle’s Q2 2025 earnings beat expectations and sent the stock up 7%, briefly touching 159post−release. Revenue came in at 658 million, a 53% increase year-over-year — certainly a number that's hard to ignore. But despite the strong headline figures, the story isn’t as straightforward as it looks. There’s still a wide gap between Circle’s long-term ambitions and where it stands today.

By the end of Q2, USDC’s circulation had reached 61.3 billion. That figure rose to 65.2 billion by August 10— a 6% quarter-over-quarter increase. Not bad… but to hit management’s ambitious 40% annual growth target for USDC, Circle would need to nearly double that growth rate to 11.6% per quarter in the second half of the year.

Circle’s IPO in June 2025 was widely viewed as a landmark moment for the stablecoin industry, and USDC’s 6% growth in this context isn’t incredible. But unless Circle can demonstrate faster adoption — especially in payments — there’s a risk those expectations won’t materialize fast enough.

Circle is thinking bigger. In 2024, it launched EURC — a fully-regulated euro-backed stablecoin out of France. It’s now the largest euro-denominated stablecoin in terms of circulation, with a market cap of $225 million — nearly triple what it was a year ago. So international expansion is clearly part of the plan.

CoinMarketCap, EURC market cap, data as of August 20, 2025.

The current market environment still lacks broad, real-world adoption of stablecoins — so a short-term slowdown in growth may not be the real issue here. What matters more is whether Circle can successfully break into cross-border and institutional payment use cases to expand its market share. That’s the kind of traction that could unlock stronger, more sustainable long-term growth.

Building the Payments Engine

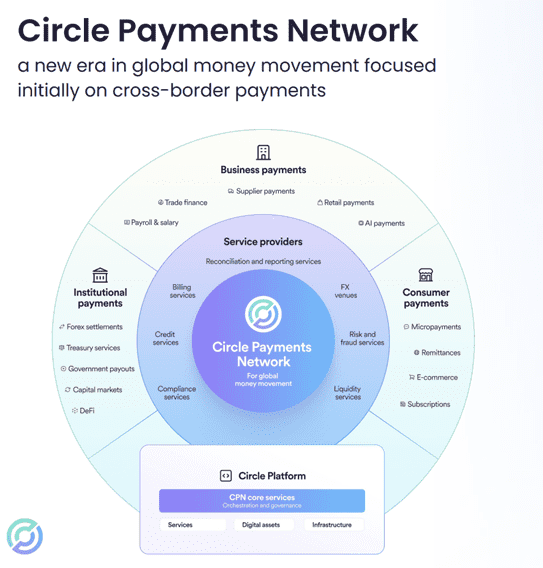

To help solve that, look at Circle’s recent moves in the global payments space.

Back in May, Circle launched the Circle Payments Network (CPN), a stablecoin-based platform for cross-border transactions. So far, it’s live in four markets — Hong Kong, Brazil, Mexico, and Nigeria — and has four active partners: RedotPay, Conduit, Tazapay, and Alfred. Over 100 more partners are in the pipeline. Circle expects the network to pick up real momentum in the second half of 2025.

CPN isn’t just about adoption — it’s starting to generate revenue, too. That includes transaction fees, network access charges, and FX spreads. A positive sign that Circle’s infrastructure bets are starting to pay off.

Circle also introduced a new blockchain called Arc — a custom-built Layer-1 chain aimed at payments, FX, and capital markets. Arc is fast (sub-second settlement), secure, and designed to meet key financial regulations, including Basel standards. USDC will be the native gas token, meaning users will pay network fees in USDC — another non-interest-based source of income that could become meaningful over time.

Other Revenue is Small — But Has High Potential

Circle’s “other revenue” — which includes things like blockchain rewards, cross-chain transfers, redemption fees, and yield product revenue (like from USYC) — came in at 24 million for the quarter, comfortably beating estimates of 17 million.

Management raised its full-year guidance for this category to 75–85 million, up from70 million. Though small today, this revenue type has high margins and supports infrastructure growth. Over time, it could be a key component of Circle’s transition from relying heavily on interest income to generating platform-based revenue.

They're playing the long game, and this is foundational stuff.

Circle’s Q2 Earnings Are Coming—Here’s What Investors Should Be Watching

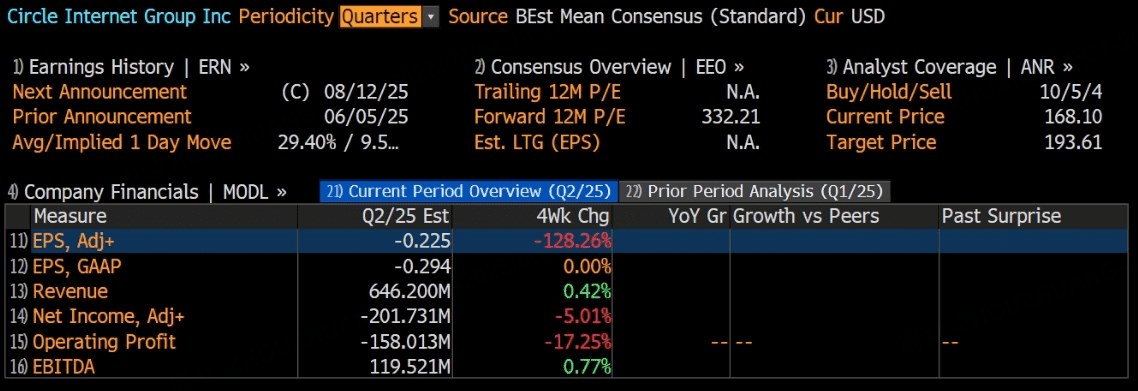

TradingKey - Since its IPO in June, Circle has been in the spotlight. As the second-quarter earnings release (scheduled for August 12) approaches, investors are wondering: Can Circle keep up the momentum it showed in Q1?

Circle’s Business: Making Money Off the “Interest Spread”

At its core, Circle has a pretty straightforward model. When users want to get USDC — the stablecoin tied 1:1 to the U.S. dollar — they send dollars to Circle. That’s called “minting” USDC.

What does Circle do with the cash? It deposits the dollars into custodial reserve accounts, mostly invested in short-term U.S. Treasuries and other low-risk assets. The interest earned on these reserves is Circle’s main source of revenue.

When users want their dollars back, they “redeem” USDC. The token is burned, and the fiat goes back into their bank account. Circle keeps the interest in the middle — it’s essentially earning a spread by holding assets that yield more than the cost of managing the system.

Strong Growth, But Costs Are Catching Up

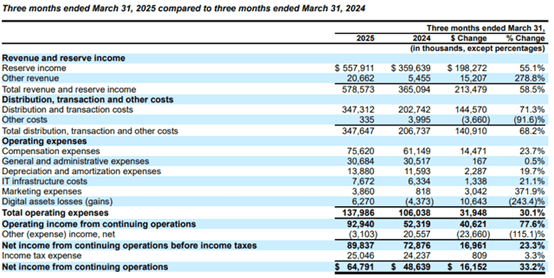

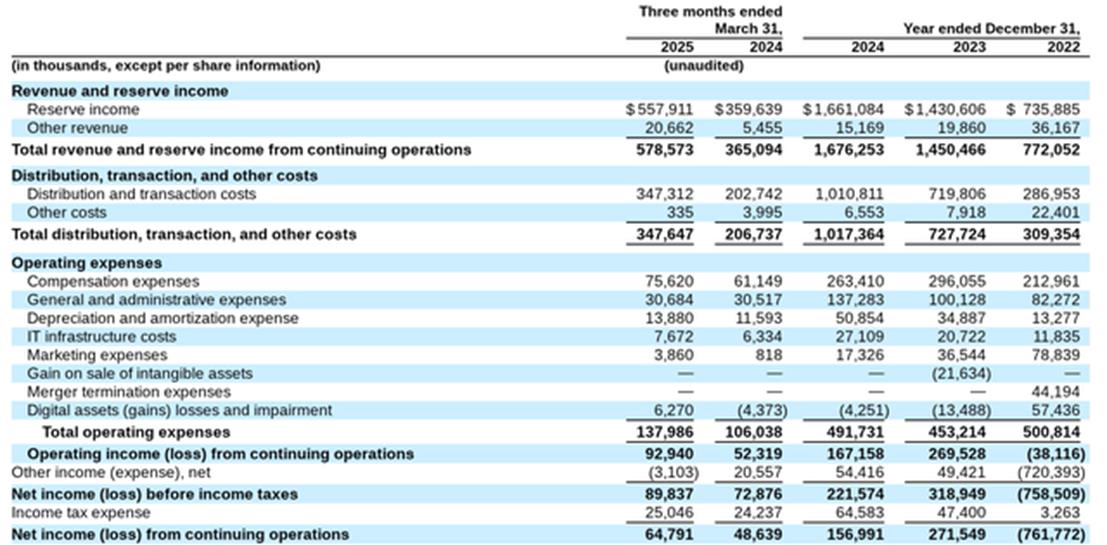

Circle’s Q1 FY2025 numbers were solid: reserve income jumped 55% YoY. That kind of growth was driven by rising demand for USDC and high interest rates on reserves.

But growth came at a cost. Literally. Total expenses grew by 73% YoY — that’s faster than revenue, and it squeezed margins.

Much of that increase had to do with distribution costs, especially fees paid to Coinbase, Circle’s biggest distribution partner. More on that in a minute.

Meanwhile, regulatory clarity has been boosting institutional confidence in USDC. That trend is expected to support continued adoption. Analysts are calling for Q2 revenue to grow around 55% YoY, though sequential (QoQ) growth will probably be more moderate — around 10–15%. Bloomberg’s consensus has Q2 revenue pinned at about $646 million.

Circle isn’t standing still. In 2024, it launched EURC, a euro-backed stablecoin. It’s still early, but the feedback has been positive. Over time, EURC might help Circle expand its footprint into new markets.

Bigger picture, the company is building out a global blockchain-based payments infrastructure: the Circle Payments Network (CPN). The idea is to enable near-instant, low-cost, cross-border payments using stablecoins like USDC and EURC.

Right now, CPN isn’t a revenue machine — but investors see it as a strategic bet that could reduce Circle’s reliance on intermediaries, lower operating costs, and potentially unlock a new revenue stream as it scales.

Trying to Break Free from Coinbase: Enter Binance and Others

Despite strong revenue growth, Circle has yet to turn those dollars into steady profits.

What’s dragging it down? Distribution fees — particularly those paid to Coinbase under their revenue-sharing agreement.

Here’s the issue: Coinbase gets 100% of the interest income earned on USDC held on its platform and a 50% cut from reserves held elsewhere. With about 20% of all USDC sitting on Coinbase, that's a pretty sweet deal — for Coinbase.

In fact, according to JPMorgan, Coinbase made about 300 million from USDC in Q1 —more than Circle’s net income of 230 million. That’s a tough pill to swallow and underscores Circle’s current channel-dependency problem.

Circle knows it can’t rely too heavily on one partner. In 2024, it struck a deal with Binance — paying a 60million one−time fee plus monthly SOFR−based payments—to secure 1.5 billion of USDC liquidity support.

It’s also integrating with wallets, blockchain networks, and other platforms to create more diverse on-ramps. That said, Coinbase still dominates — newer partners haven’t yet contributed enough to change the picture meaningfully.

Looking ahead, distribution costs are still expected to trend higher in Q2, but not as sharply as in Q1. Circle’s actively trying to balance growth with smarter spending. Success in scaling CPN could eventually help ease the pressure on margins and change how Circle reaches users altogether.

Profitability Outlook: Still in Limbo

As of now, Circle’s bottom line remains fragile. In Q1, gross profit clocked in at 230 million—but net EPS came in right at 0.00 due to high costs.

Analyst expectations for Q2 are all over the map. Some forecasts suggest losses in the range of 0.08–0.08–1.29 per share; others think Circle might squeeze out a small profit — up to $0.20 per share. Regardless, stable and meaningful profitability likely won’t happen until Circle finds a way to materially bring distribution costs down or generate scalable revenue from new initiatives like CPN.

Pre-Profit and Still a Buy? Let’s Talk Valuation

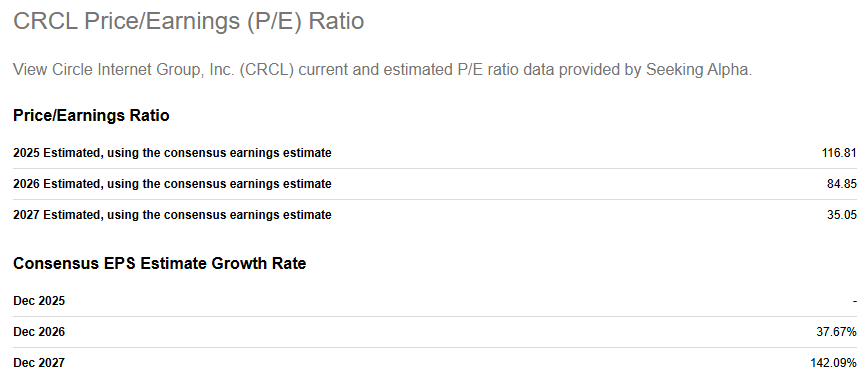

Let’s now turn to the investment perspective. Circle (CRCL) currently trades at a forward P/E of 117 — high on paper, but not unusual for a young, fast-growing company. Early-stage firms often lack near-term profits, but valuations reflect strong expectations for future growth.

According to Seeking Alpha, Circle’s EPS is projected to grow 38% in 2026, and nearly 150% in 2027. If achieved, its forward P/E could drop to around 35 by 2027 — a much more reasonable level relative to earnings.

This shift suggests two things: 1) Profitability is expected to accelerate; 2) The current stock price may not fully reflect future earnings power.

So while Circle isn't yet highly profitable, strong growth potential gives its current valuation context — and possible upside for long-term investors.

After Circle’s IPO Surge and Pullback — Buy the Dip or Exit?

TradingKey - After a blockbuster IPO, Circle—the company behind the USDC stablecoin—saw its stock price skyrocket to 8x its offering price on the first day of trading. But fast forward two weeks, and sentiment has cooled off. The stock is now consolidating around $150, leaving investors asking the big question:

Is this dip a golden entry point—or is it time to cash out and de-risk?

What Makes Stablecoins More Than Just a Crypto Fad?

While some still see stablecoins as just another crypto offshoot, they’re gaining serious traction as a potential evolution of fiat money. With benefits like instant settlement, no middlemen, near-zero transaction fees, irreversible transactions, programmability, and full transparency, stablecoins are shaping up to be a major player in global finance—not just crypto.

So, why are people actually using them?

It comes down to three things every user cares about—safety, speed, and cost. Most people don’t actually care if it’s a “stablecoin” under the hood. They care if their money arrives safely, quickly, and without high fees. As Higlobe co-founder Farman-Farmaian put it: users only care about outcomes, not what token powers that outcome.

And this is exactly where stablecoins shine—especially for cross-border payments. Because they’re pegged 1:1 to the U.S. dollar, users don’t have to worry about FX volatility. USDC, in particular, stands out. It's backed by cash and short-term treasuries—making it one of the most transparent and liquid options in the space. Compare that with USDT (Tether), which has a murky reserve mix (including loans, crypto, and even precious metals) and a history of regulatory scrutiny.

In short, USDC addresses real-world pain points in cross-border finance: it’s fast, safe, and cheap.

The Market Is Big—and It’s Getting Bigger

We’re just scratching the surface. Even if stablecoins only capture a sliver of the global financial system, the upside is massive. According to a joint report from Standard Chartered and Zodia Markets, stablecoins could account for 10% of the U.S. money supply and global FX volume by 2035.

USDC currently owns about 28% of the stablecoin market. If Circle can maintain or grow that share, its revenue could one day rival that of Visa—yes, the $600 billion payments giant.

.png)

Right now, most of the demand is flowing from emerging markets.

In regions like Africa, Latin America, and Southeast Asia, access to stable financial infrastructure is limited. From individuals looking to hedge against local currency volatility, to small businesses struggling to make cross-border payments, stablecoins (especially USDC) offer an appealing alternative.

It started with crypto-native firms moving capital around blockchain ecosystems. But now, large multinationals are paying serious attention. Use cases are evolving rapidly, and one breakout scenario tends to lead to more. Demand is compounding.

But What's the Catch? It’s Not All Smooth Sailing

Yes, stablecoins are promising—and USDC is a top contender. But Circle’s business model has its weak spots.

First, let’s talk about revenue. Circle makes money by investing the dollars backing your USDC into U.S. Treasuries and other low-risk instruments. That interest goes to Circle—not to you. So effectively, Circle gets access to billions in “zero-interest” capital. Not a bad deal—unless interest rates start heading south.

And that’s exactly what markets are anticipating. With the Fed widely expected to begin a rate-cutting cycle, Circle’s yield on those reserves could shrink fast.

Now add competition into the mix.

Some upstart stablecoins are shaking things up by offering yield directly to holders. That puts pressure on Circle’s “no-interest-to-users” model and could redirect institutional flows away from USDC over time.

There’s also a strategic pivot underway. Circle is branching out into non-USD stablecoins—including the newly launched EURC, pegged to the euro. A smart long-term move, but still early days in terms of uptake.

Then there’s the tricky part: its partnership with Coinbase.

Circle and Coinbase co-founded USDC, and under current agreements, Coinbase gets a big chunk—up to 60%—of the revenue generated from USDC, primarily for distribution and promotion. That eats into Circle’s margins in a big way.

Even more concerning? If Circle is ever unable to meet certain obligations or faces regulatory issues, Coinbase has the contractual right to become the sole issuer of USDC. That’s not just a revenue problem—it could undermine Circle’s entire role in the ecosystem.

To offset this, Circle is reportedly renegotiating its revenue-sharing structure and attempting to build its own distribution stack. Easier said than done—and whether the market will accept a new distribution pathway remains to be seen.

Conclusion

At a high level, Circle still looks positioned as a key player in the evolution of digital finance. With compliant infrastructure, institutional-grade reserves, and rising real-world utility, USDC could continue to expand across both emerging economies and enterprise use cases.

But the long-term opportunity has some near-term execution risks.

Revenue is heavily tied to interest rates and dependent on a profit-sharing model that may not be sustainable. Meanwhile, competition is heating up fast.

The IPO hype has settled—but that doesn’t mean the story’s over. This correction may be less about weakness and more about recalibration. For mid- to long-term investors, it’s an ideal window to reassess: does Circle really have the fundamentals, strategy, and moat to grow into a $600 billion narrative?

The company wants to become the “Visa of Web3.” The next chapter will show whether that’s vision—or vapor.

推荐文章

美股机会日报 | 经济数据强劲!美国1月非农就业大超预期,纳指期货涨至0.6%;AI应用股业绩超预期,Shopify涨超10%

资金复盘 | 北水净买入港股超48亿港元,逾7亿港元抢筹腾讯

华盛早报 | “AI威胁”波及华尔街!财富管理公司全线暴跌;豆包官宣“参战”!春节AI红包战愈演愈烈

美股机会日报 | 科技巨头迎利好?特朗普政府拟结构性豁免芯片关税;台积电1月销售额创历史新高,盘前股价涨近3%

一图看懂 | 净利大增60.7%!中芯国际Q4营收24.9亿美元,同比增长12.8%

美股机会日报 | 市场风格趋变?美银称接下来是小盘股的天下;金价重回5000美元上方,贵金属板块盘前齐升

新股暗盘 | 乐欣户外飙升超70%,中签一手账面浮盈4345港元;爱芯元智微涨超0.2%

高盛预计英伟达Q4营收达673亿美元 给出250美元目标股价